Pernod Ricard SA

An In-Depth Analysis of the Business Model

Executive Summary

Pernod Ricard SA, a global leader in the spirits and wine industry, boasts a robust portfolio of premium to luxury brands that positions it at the forefront of the global structural premiumization trend. For the fiscal year ended June 30, 2025, the company reported consolidated sales of €10,959 million, reflecting a 3.0% organic decline amid normalization in the United States and challenging macroeconomic conditions in China. Despite these headwinds, the group achieved an organic operating margin expansion of +64 basis points, reaching 26.9%, underpinned by the completion of a €900 million efficiency program and disciplined cost management.

The company is transitioning from a period of peak strategic investment in aging inventory and production capacity toward a phase focused on cash conversion and operational agility. Beyond the high-profile recruitment of younger cohorts, Pernod Ricard is increasingly positioned to benefit from a defining demographic shift: the expansion of the “Silver Economy.” Within its key markets, the population aged 65 and above is projected to grow by 36% through 2035, representing a resilient and high-disposable-income segment. With a medium-term objective of 3% to 6% organic sales growth and a Return on Invested Capital (ROIC) of 7.1%, Pernod Ricard leverages its decentralized “Conviviality Platform” and industry-leading distribution to secure long-term value.

Pernod Ricard is a premium spirits powerhouse transitioning to a high-efficiency model that captures both the aspirational growth of emerging-market youth and the resilient wealth of an aging global population.

1. What They Sell and Who Buys

Pernod Ricard manages a sophisticated “House of Brands” architecture, comprising 240 premium brands organized to capture a wide spectrum of consumer occasions and price points. The portfolio is categorized into four strategic segments designed to optimize resource allocation and market penetration.

1.1. Brand Hierarchy and Portfolio Segmentation

The company’s brand hierarchy is structured to maximize the “Price/Mix” ratio, shifting consumers toward higher-value products as their disposable income and taste profiles evolve.

The performance of these categories varied in recent cycles. In FY25, the Strategic International Brands saw a decline of 6%, heavily impacted by Martell’s performance in China and Global Travel Retail. Conversely, Specialty Brands like Bumbu have exhibited exceptional resilience, with Bumbu achieving double-digit growth and becoming the world’s #1 super-premium rum.

1.2. Regional Consumption Dynamics and Target Demographics

Pernod Ricard’s customer base is increasingly defined by the expansion of the middle and affluent classes in emerging markets and shifting values in mature economies.

In Asia and the Rest of the World, which accounts for 42% of group sales, the primary driver is the burgeoning middle class. An estimated 1.5 billion consumers in Asia are expected to enter the middle class between 2020 and 2030, seeking “status” brands as symbols of individual expression and social advancement. In India, the company recruits 20 million people who reach the legal drinking age every year, a demographic that is increasingly opting for international premium spirits over traditional domestic options.

In mature markets like the United States (19% of sales) and Europe (29% of sales), the consumer base is fragmenting. Pernod Ricard focuses on individuals aged 25 and above, particularly urban professionals with disposable income. The “Legal Drinking Age to 27” cohort (Gen-Z) in these regions is increasingly health-conscious and values authenticity and sustainability. Spirits penetration among US Gen-Z grew from 71% in 2018 to 74% in 2023, indicating a shift toward mixability and higher-quality options over mass-market beer.

1.3. Purchase Motivations and Occasions

Pernod Ricard’s “Conviviality” model identifies specific “Moments of Consumption” (MOCs) to tailor its brand offerings.

Social Enthusiasts and Special Occasions: Consumers purchasing Prestige brands like Royal Salute or Perrier-Jouët are driven by status, heritage, and the desire for unique, memorable experiences.

Experiential Consumption: The on-trade channel (bars and restaurants) accounts for 56.7% of global premium spirits revenue, where motivations are centered on the “experience” of a professional cocktail or a social gathering.

Smart Spending and Home Entertainment: High inflation in mature markets has led to a “smart spending” trend where consumers drink less frequently but choose higher-quality spirits for home consumption. This has benefited brands like Kahlúa and Jameson, which have high utility in at-home cocktail making.

2. How They Make Money

The company’s revenue generation is built upon a decentralized business model that integrates production, global brand building, and a wholly owned distribution network.

2.1. The Value Chain and Maturation Process

Revenue is fundamentally linked to the aging and maturation of spirits, a process that creates a significant barrier to entry and inherent value growth.

The production cycle begins with sourcing raw materials from approximately 380,000 hectares globally. While most of the raw materials are sourced, Pernod Ricard retains high-value holdings essential for prestige brands, including 450 hectares in Cognac (Domaines Jean Martell) and 260 hectares in Champagne (Mumm and Perrier-Jouët). By managing its own distilleries and vineyards, the company ensures quality control from “grain to glass”. A critical component of the financial model is the management of “aged work in progress” inventory. As of June 30, 2025, the company held €7,062 million in maturing inventory, an increase from €6,616 million in 2024. This inventory matures in barrels for years (e.g., Scotch, Cognac, Irish Whiskey), during which its market value appreciates. The ability to forecast demand 10 to 20 years in advance and manage the associated capital tie-up is a core competency that defines the company’s profitability.

2.2. The Distribution Network

Pernod Ricard captures a larger portion of the value chain by owning its distribution network in 73 to 75 markets and having a presence in over 160 countries. This direct-to-market approach allows for faster reaction to local trends and more effective pricing strategies compared to competitors who rely on third-party distributors.

2.3. The “Conviviality Platform”

Management has transitioned the company into a data-led organization via the “Conviviality Platform.” This model uses artificial intelligence and proprietary data to drive revenue growth in several ways:

Demand Analysis: Utilizing Key Digital Programs (KDPs) to analyze consumer needs and moments of consumption across 28 markets covering 75% of group sales.

Portfolio Optimization: Using the “Matrix” tool to allocate advertising and promotional (A&P) spend dynamically to the brands and markets with the highest marginal return.

Retail Execution: The “D-STAR” tool provides the sales force with granular insights and “Execution Alerts,” optimizing outlet-level sales and shelf placement.

The “Conviviality Platform” provides 3,000 daily alerts to optimize sales force performance.

3. Revenue Quality

Revenue quality at Pernod Ricard is underscored by strong brand equity, geographical diversification, and the ability to maintain market share even in volatile environments.

3.1. Market Share

The company is gaining or maintaining value market share in 12 of its top 17 markets. This performance indicates that the company’s brands are outperforming the broader industry, even when category volumes are under pressure.

India: Jameson has become the #1 imported spirit brand in the country, and India is now the second-largest market for Jameson by volume globally.

United States: While organic sales declined 6% in FY25, Pernod Ricard is “narrowing the gap-to-market”. Brands like Jameson, Absolut, and Kahlúa are performing ahead of their competitive sets, reflecting sharp execution and effective brand investment.

China: Despite the 21% decline in FY25, Pernod Ricard holds a 42% value market share in international premium spirits. The long-term equity of Martell remains high, and the company is successfully recruiting the new middle class through premium brands like Absolut and Olmeca, which saw strong growth.

3.2. Pricing Power

A hallmark of premium spirits revenue is the ability to pass through cost increases to consumers. In FY24, the company achieved organic gross margin expansion of +108bps, driven by pricing discipline and operational efficiencies. In FY25, despite the top-line decline, the company achieved organic operating margin expansion of +64bps. This demonstrates that the company can protect its bottom line by focusing on “value over volume” and utilizing its premium brand positioning to maintain price levels even as volumes fluctuate.

3.3. Diversification

The broad-based geographic footprint serves as a natural hedge. While China and the US (traditionally the engines of growth) were soft in FY25, many other markets posted resilient to strong growth:

Turkey and South Africa: Very strong organic and reported sales growth led by Chivas Regal and Jameson.

Western Europe: Growth in France offset declines in Germany and Spain, while the company maintained share in the UK and gained share in Poland.

Global Travel Retail (GTR): Although GTR Asia was impacted by the suspension of Cognac imports in China Duty Free, GTR globally is expected to gradually improve as passenger numbers normalize and Chinese travelers recover.

3.4. Revenue Vulnerabilities

Revenue quality is currently being tested by several “cyclical” rather than “structural” headwinds:

Distributor Inventory Adjustments: High interest rates in the US have led distributors to lower their inventory levels to preserve cash, a process expected to continue through FY26.

Anti-Dumping Investigations: The ongoing investigation by Chinese authorities into European Cognac imports has created an overhang of distributor inventory and impacted trade sentiment.

Normalization of Consumption: Following two years of “outsized growth” post-COVID, consumption patterns are returning to historical mid-single-digit CAGRs (e.g., 5% Group Sales CAGR from FY19-FY24).

4. Cost Structure

Pernod Ricard’s cost structure is characterized by a high degree of investment in brand building, balanced by an aggressive operational efficiency program.

4.1. Advertising and Promotion (A&P) Strategy

A&P is the group’s largest discretionary expense, consistently maintained at approximately 16% of net sales. This ratio is central to the company’s strategy of “investing in brand desirability” to ensure long-term sustainable growth.

In FY24, A&P spend was €1,872 million. For FY25, the company prioritized the US market through “sharper marketing resource allocation” to maximize growth opportunities in a competitive landscape. The shift toward digital channels—representing over 75% of paid media budget—allows for higher precision and measurable ROI.

4.2. Operational Efficiency

The company has successfully used large-scale efficiency programs to expand its operating margins.

FY23-25 Efficiency Program: Successfully completed in FY25, delivering €900 million in cumulative savings. This program was a primary driver of the +64bps organic operating margin expansion in FY25.

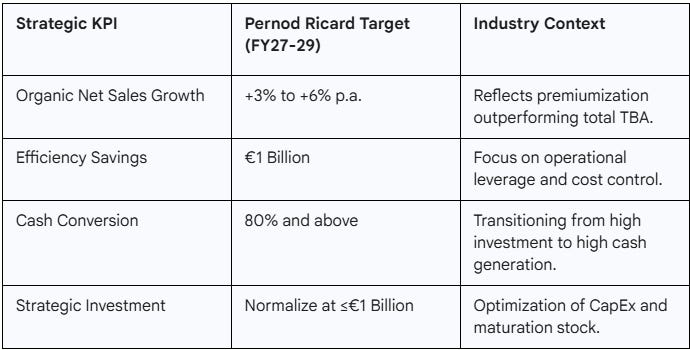

FY26-29 Program: A new €1 billion efficiency target has been set for the next four fiscal years. This program aims to optimize operations and implement a “Fit for Future” organization based on simplification, empowerment, and discipline.

4.3. Structure Cost and COGS Management

Structure costs (personnel, administration, and support) were reduced organically by 2% in the first half of FY25 through strict discipline and continuous improvement. Cost of Goods Sold (COGS) are also being optimized through efficiency programs focused on logistics and procurement.

The disposal of lower-margin businesses is another structural lever. The sale of the Imperial Blue business in India and the strategic wine brands is expected to be immediately accretive to the group’s overall gross and operating margins. For example, disposals of non-core brands are estimated to add approximately +260bps to Gross Margin and +80bps to Operating Margin in the medium term.

4.4. Foreign Exchange and Macroeconomic Impacts

Pernod Ricard is highly exposed to currency volatility. In FY24, a negative FX impact of €784 million was reported, primarily linked to the Argentine Peso, Turkish Lira, and US Dollar. In FY25, the negative FX impact was €277 million.

While organic margin expansion is robust, the reported margin is often “sustained” rather than increased due to significant adverse FX impacts. Management expects FX impacts to remain “significantly negative” for the foreseeable future.

5. Capital Intensity

The spirits business is inherently capital-intensive due to the requirement for physical production assets and the multi-year maturation of inventory. However, Pernod Ricard is entering a period of normalization after a multi-year investment peak.

5.1. Aging Stock

Pernod Ricard’s balance sheet is dominated by “Aged Work in Progress” inventory, which increased from €6,616 million in June 2024 to €7,062 million in June 2025. While this represents a high level of capital tie-up, the company noted that investments in these strategic inventories “passed their peak in FY24”.

The net acquisitions of strategic inventory decreased from €640 million in FY24 to €537 million in FY25. For the medium term (FY27-29), the company expects strategic investments (inventories and CapEx) to normalize at no more than €1 billion per year, down from the recent highs of €1.2 billion in FY24/25.

5.2. CapEx and Cash Conversion

CapEx has similarly moved past its peak. Net acquisitions of non-financial assets declined from €764 million in FY24 to €655 million in FY25.

The company’s focus has shifted toward “Cash Conversion Efficiency.” Free Cash Flow (FCF) reached €1.133 billion in FY25, an 18% increase (+€170 million) compared to FY24. This improvement was driven by:

Strong operating working capital management, particularly an improvement in finished goods inventory.

Management’s goal is to achieve a cash conversion rate of 80% and above in the medium term (FY27-29) to fund financial policy priorities.

5.3. Debt and Financial Position

Pernod Ricard maintains a solid investment-grade rating: BBB+ (stable) by S&P and Baa1 (stable) by Moody’s.

Net Debt: Decreased by €224 million to €10,727 million by the end of June 2025, benefiting from improved FCF and a weakening US Dollar.

Leverage: The Net Debt/EBITDA ratio rose slightly from 3.1x to 3.3x in FY25, primarily due to the negative impact of foreign exchange on recurring profit rather than an increase in debt.

ROIC: FY25 ROIC was approximately 7.1% (normalized), up from 6.8% in FY24. This reflects the high capital tie-up of maturation stock, though the trend is improving as the group divests lower-return wine assets.

6. Growth Drivers

Long-term growth is predicated on global premiumization, expansion in emerging markets, and technological leadership in consumer engagement.

6.1. The Premiumization Trend

The global spirits market is evolving from volume-driven to value-driven growth. While total beverage alcohol volumes declined by 1% in 2024, premium-and-above volumes grew by 3%. Pernod Ricard is ideally positioned to benefit from this shift, as its portfolio is heavily weighted toward the “Super-Premium” and “Ultra-Premium” categories, which are growing at faster rates than the “Standard” or “Value” segments.

6.2. India and China

The company’s “Must-Win” strategies in India and China are central to its 2030 roadmap.

India: The country is witnessing a “home-grown spirit” revolution alongside strong demand for international brands. The premiumization of the Seagram’s portfolio (led by Royal Stag and Blenders Pride) and the success of Jameson (the #1 imported spirit) provide a massive long-term tailwind. The disposal of the Imperial Blue business allows the company to focus exclusively on these higher-margin segments.

China: Despite short-term volatility, the rise of the middle class is non-negotiable. Pernod Ricard is localizing its presence with “The Chuan,” the first prestige malt whisky produced by an international group in China, and is expanding into the growing “home consumption” and “home entertainment” occasions.

6.3. RTDs and Non-Alcoholic

Pernod Ricard is successfully tapping into new consumption moments to capture the “Total Beverage Alcohol” (TBA) share.

Ready-to-Drink (RTD): RTD cocktails and long drinks are forecast to double globally between 2019 and 2029. Pernod Ricard aims to triple its RTD footprint in the US over the next three years, leveraging the equity of brands like Absolut and Jameson.

Non-Alcoholic Spirits: The non-alcoholic volume segment grew by 6% in 2023, driven by a mainstream shift toward moderation. Pernod Ricard’s innovations, such as Ramazzotti Arancia 0, are already gaining significant market share in Europe.

6.4. The “Silver” Economy

The 65+ demographic will be a defining force for decades. Demographics are dominated by China and India, whose 65+ populations will be more than double those of the other top five key markets combined by 2035. This cohort’s alcohol penetration is rising (e.g., U.S. 55+ segment up 10 percentage points in two decades), offering a massive, stable pool for premium and heritage brands.

6.5. Digital Transformation and AI

The “Conviviality Platform” represents a second-order growth driver by improving the efficiency of every Euro spent. The group allocates over $1.2 billion annually to online channels, funding targeted campaigns and influencer partnerships. By the end of 2025, the company had connected with 1 billion young adults digitally. This digital-first customer acquisition strategy, combined with the “Matrix” and “D-STAR” tools, is expected to drive organic net sales growth toward the medium-term range of +3% to +6% per annum.

7. Competitive Edge

Pernod Ricard’s competitive advantage resides in its “dual leadership” in key markets, its industry-leading distribution network, and its commitment to sustainability as a business driver.

7.1. Portfolio Breadth and Category Diversity

Pernod Ricard holds the most complete portfolio of actively managed premium international spirits in the industry. Unlike competitors who may be dominant in only one or two categories (e.g., Diageo in Scotch and Tequila), Pernod Ricard has leadership positions in:

Irish Whiskey: Jameson (#1).

Anise-based Spirits: Ricard (#1).

Malibu Rum: World’s best-selling coconut-flavored rum.

Cognac: Martell (#1/2 globally).

Super-Premium Rum: Bumbu (#1).

This breadth mitigates category-specific risks and allows the company to pivot resources toward whatever category is trending in a given region.

7.2. Global Distribution Moat

The company’s wholly owned distribution network is a formidable barrier to entry. With 60 in-house sales teams covering 160 countries, Pernod Ricard can execute global brand launches (like Skrewball or Bumbu) with unparalleled speed and consistency. This infrastructure also provides the company with deep local insights that are fed back into the “Conviviality Platform,” creating a virtuous loop of data and execution.

7.3. Corporate Culture

The ‘Art of Conviviality’ culture is a unique intangible asset. With 18,500 employees acting as “ambassadors of authentic conviviality,” the company maintains high levels of employee engagement, which facilitates the decentralized execution required for a global spirits business. The group has also achieved gender pay equity and balanced top management, reflecting its commitment to a modern, inclusive corporate structure.

7.4. Financial Framework Comparison

Compared to its primary direct competitor, Diageo, Pernod Ricard offers a more balanced geographic profile, particularly with its stronger relative positioning in Asia. While Diageo has historically seen stronger growth in Tequila, Pernod Ricard’s recent acquisitions (Código, Olmeca) and its leadership in the “International Premium Plus” sector provide it with a robust engine for the next phase of the spirits cycle.

Conclusion

Pernod Ricard is an expertly managed, high-quality enterprise that is successfully navigating a normalization period in the spirits industry. Its transition toward a more efficient, cash-generative model, combined with its dominant positions in emerging markets and high-growth categories, provides a compelling narrative for long-term investors seeking exposure to the global consumer luxury and conviviality trends.

Thanks for reading!

Stiliyan Loukanov, Feather Fund

Open an account with Interactive Brokers to support the blog:

https://ibkr.com/referral/stiliyan756

Sign up to Revolut with the link below to support the blog:

ttps://revolut.com/referral/?referral-code=stiliyujwu!MAY1-24-AR

Open an account with eToro to support the blog:

Disclaimer: The information presented here, including ideas, opinions, views, predictions, forecasts, commentaries, or suggestions, whether explicitly stated or implied, is intended purely for informational, entertainment, or educational purposes. None of the content should be interpreted as personalized investment or financial advice. Although every effort has been made to ensure the accuracy of the information provided, errors or inaccuracies may be present. Always exercise caution and seek professional financial advice before making any investment decisions.