Interparfums, Inc.

An In-Depth Analysis of the Business Model

• Company name: Interparfums, Inc.

• ISIN: US4583341098

• Ticker: IPAR

• Stock Price: 92.46 USD

• Market cap: 3.01B USD

• Average daily volume: 263,638 USD

Executive Summary

Inter Parfums, Inc. (IPAR) operates as a highly specialized global enterprise in the prestige fragrance sector, fundamentally driven by an asset-light, intellectual property-focused licensing model. Since 1982, the company has focused on securing exclusive worldwide license agreements to manage the creation, production, and distribution of fragrance and related products for prominent fashion and luxury brand owners. The strategy positions IPAR as an “IP arbitrageur,” leveraging its operational expertise to convert the enormous brand equity of global fashion houses into high-margin, predictable cash flow streams. This approach insulates the company from the immense capital expenditures (CapEx) and supply chain inventory risks typically associated with vertically integrated conglomerates in the luxury goods sector.

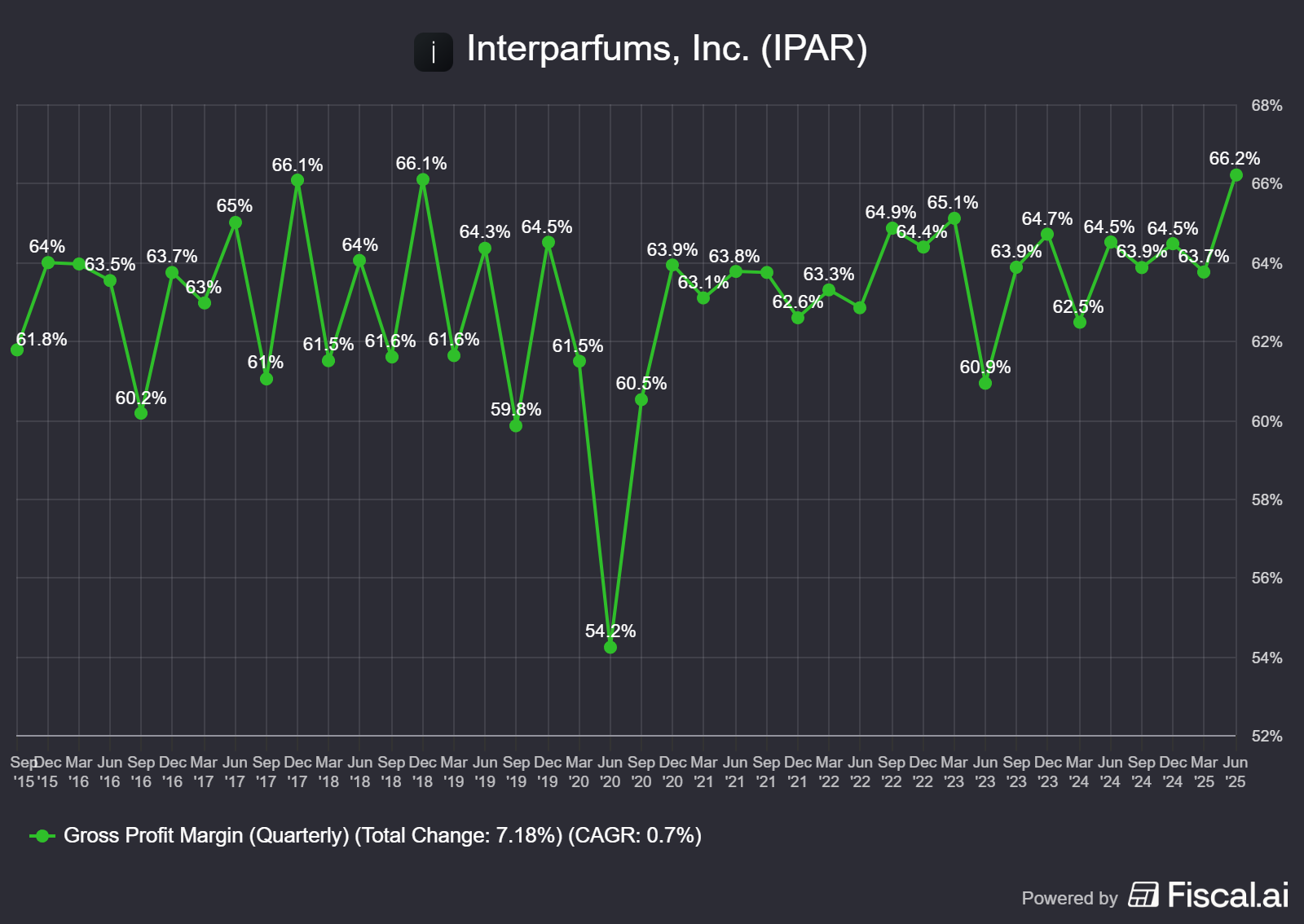

The business model has demonstrated exceptional financial resilience and effective management control, as evidenced by the reported results for H1 2025. Notably, the Gross Margin expanded significantly by 170 basis points (bps) in Q2 2025 to reach 66.2%, indicating superior command over product sourcing and outsourced manufacturing costs, even amidst volatile consumer sentiment. This consistently high profitability, supported by a strong cash position ($205 million as of H1 2025), enables the company to pursue strategic, long-term IP acquisitions, such as the Longchamp license, which extends until 2036.

The structural competitive advantages of the asset-light approach provide operational agility; however, the model is not without risks. The enterprise remains significantly exposed to brand concentration risk, with approximately 73% of sales derived from just six major licensed brands. Additionally, the high proportion of international sales exposes reported USD earnings to foreign currency fluctuation, notably the USD/EUR exchange rate. IPAR addresses these systemic vulnerabilities through efforts to diversify IP via both durable license renewals and the strategic development of proprietary brands, such as the recently announced Solférino collection.

I. Corporate Architecture and Market Positioning

1.1 The Dual Operating Structure

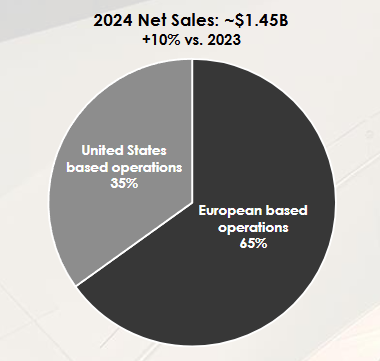

Interparfums operates under a specialized dual corporate structure designed to manage global distribution and leverage local expertise. Interparfums, Inc. manages the US-based operations, while its European-based operations are conducted through Interparfums SA (listed on Euronext: ITP), in which IPAR holds a 72% majority ownership stake.

This structure dictates the revenue segmentation and brand allocation. For the FY2024, European operations generated approximately 65% of net sales, focusing primarily on high-prestige European luxury names. This segment’s portfolio includes Boucheron, Coach, Jimmy Choo, Karl Lagerfeld, Kate Spade, Lacoste, Lanvin, Moncler, Montblanc, Rochas, and Van Cleef & Arpels. The US operations accounted for the remaining 35% of net sales in FY2024, managing brands such as Abercrombie & Fitch, Anna Sui, Donna Karan, Ferragamo, Graff, GUESS, Hollister, MCM, Oscar de la Renta, Roberto Cavalli, and Ungaro.

The 72% ownership of ITP allows IPAR to consolidate the revenues of the high-margin European subsidiary, which holds many of the most financially valuable luxury licenses. This strategic specialization and risk partitioning are key components of the model. European operations capitalize on the perceived quality and heritage of French luxury distribution networks. Conversely, the US segment provides diversification by targeting the North American mass-prestige market, utilizing different brand tiers and customer demographics. This dual listing also enables the company to attract both European investors focused on the luxury goods sector (ITP) and North American investors (IPAR).

1.2 IPAR as the Specialist Disruptor

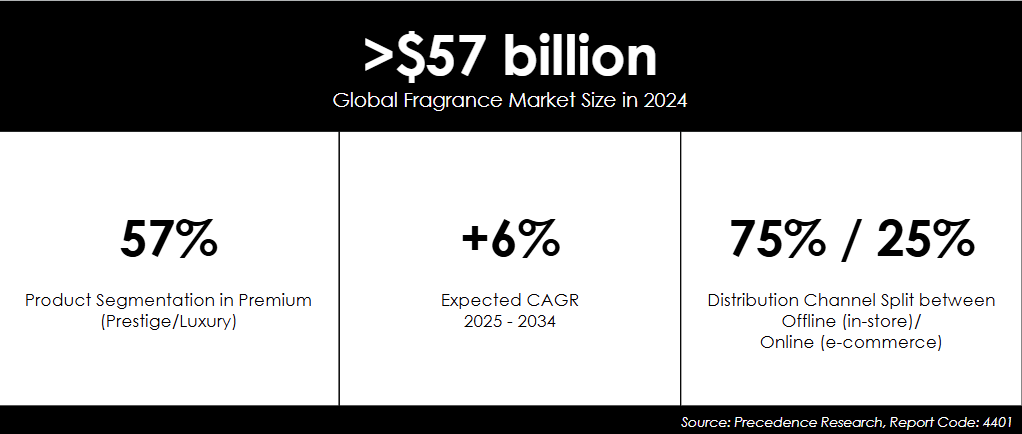

Interparfums is situated within a substantial global fragrance market, estimated at $57 billion and expected to grow at a CAGR of 6% until 2034. This growth is fueled by premiumization trends in mature markets, particularly the US and Europe, and the expansion of the affluent middle class in emerging Asian markets.

The company maintains a highly specialized competitive position, resulting in a global market share estimated at approximately 2%. This share is relatively small compared to that of large, diversified conglomerate competitors that operate vertically integrated structures: L’Oréal Luxe holds an estimated 12% market share, Estée Lauder Companies approximately 10%, and Coty Inc., approximately 7%.

IPAR’s smaller size is not a weakness but a reflection of its role as a specialized, “pure-play” agile partner. Unlike its larger peers, which must manage sprawling owned portfolios and extensive internal R&D and manufacturing infrastructures, IPAR focuses its core competency on efficiently translating a brand’s established identity into profitable fragrance lines. This specialization grants operational flexibility and allows for streamlined capital deployment focused exclusively on IP acquisition, global marketing, and expert distribution, avoiding the overhead and bureaucratic slowdowns faced by multi-category luxury houses.

II. The Asset-Light Licensing Model

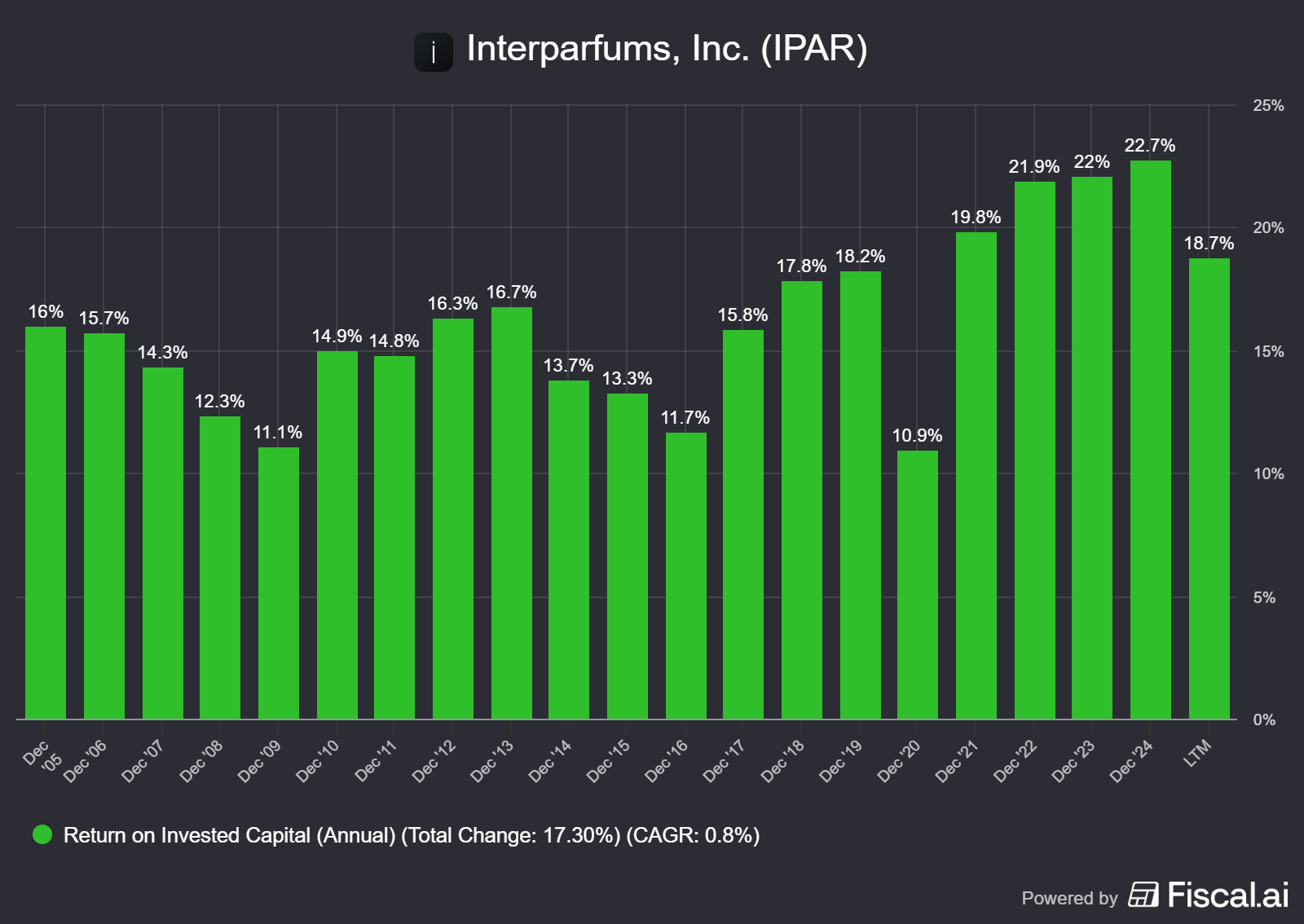

The foundation of Interparfums’ high-return model is its commitment to an asset-light structure, maximizing Return on Invested Capital (ROIC) by outsourcing capital-intensive functions and concentrating management efforts on core IP and marketing strategy.

2.1 Licensing Mechanics

The core operational model dictates that IPAR does not own any manufacturing facilities. Instead, it acts as a “general contractor,” overseeing the entire value chain from concept development (in collaboration with the brand owner and renowned perfumers) to component sourcing, final filling, global marketing, and wholesale distribution.

Licensing agreements are structured as exclusive, worldwide contracts, typically spanning five to ten years, with embedded options for renewal. The criteria for selecting a licensed brand focus rigorously on its existing market presence, growth potential, and strategic alignment with IPAR’s prestige portfolio. For instance, key current licenses such as Jimmy Choo, Karl Lagerfeld, Kate Spade, and MCM extend securely well into the 2030s.

The company’s primary expense related to brand IP is the royalty payment made to the licensor (the fashion house), calculated as a percentage of net sales. Although these rates vary by brand maturity and negotiation (e.g., Montblanc at 22%, Jimmy Choo at 16%, Coach at 14%, and GUESS at 10% in prior periods), the royalty is paid on the top-line revenue. By outsourcing all production functions, IPAR retains a high degree of commercial control over the Cost of Goods Sold (COGS). This structural arrangement allows the company to arbitrage the differential between the high perceived value of the established brand (the fixed cost input) and its low operational costs (efficient sourcing and production). This arbitrage drives the consistently high gross margins, which reached 66.2% in Q2 2025, demonstrating that the royalty expense is sufficiently lower than the net profit generated by the wholesale price spread.

2.2 Operational Resilience

IPAR’s physical supply chain and key logistics are strategically outsourced and highly concentrated geographically to maximize quality and stability. Components are sourced from suppliers and delivered to third-party fillers. This reliance is heavily centered in Europe, with approximately 80% to 85% of all purchases sourced from the continent, and 58% to 62% specifically from France. This geographical concentration demonstrates a calculated prioritization of high quality and proximity to the Parisian luxury ecosystem. The reliability of this partnership model is underscored by the longevity of these relationships, with 86% of purchases coming from suppliers with whom IPAR has worked for more than ten years.

This operational structure grants flexibility, enabling rapid scaling for new launches (such as Lacoste and Coach) while successfully mitigating the capital commitment risk associated with owning and maintaining large-scale, fixed manufacturing and warehousing assets.

2.3 Capital Structure and Return Metrics

The outsourced operational model results in a low capital intensity structure, providing significant financial flexibility. The financial position remains strong, highlighted by a large cash and cash equivalents balance of $205 million reported as of H1 2025. The small relative capital base, dominated by intangible assets (licenses and trademarks), combined with high operating profitability, inherently yields superior ROIC ratios compared to asset-heavy firms.

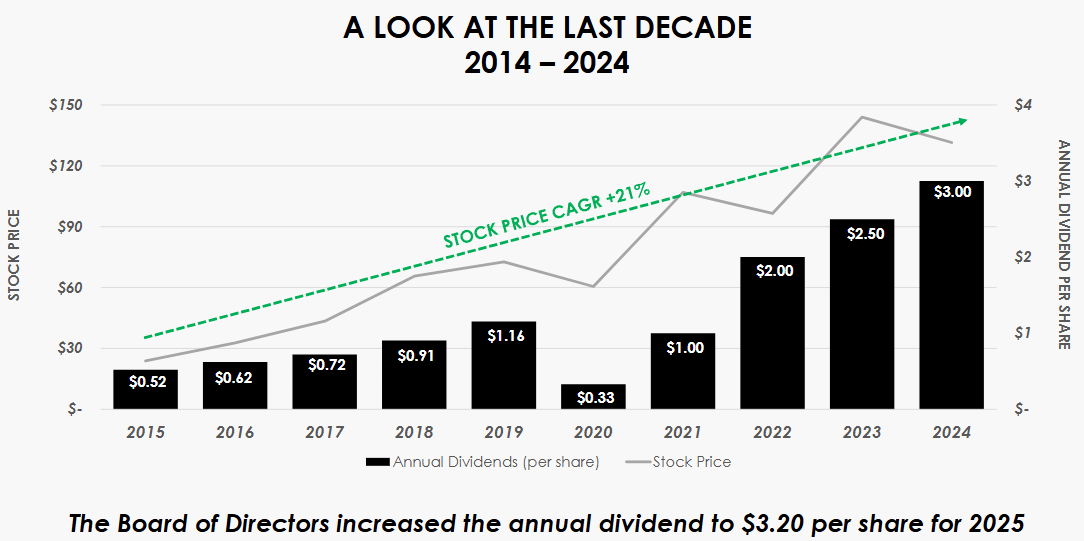

The robust operating cash flow supports a highly attractive shareholder return policy, marked by the company maintaining dividend payments for 24 consecutive years and raising dividends for five straight years.

Excess cash is strategically deployed for long-term growth initiatives, including the acquisition of new, long-term licenses (e.g., Longchamp until 2036) and internal investment in proprietary brand incubation, notably Solférino.

III. Portfolio Dynamics

3.1 Brand Portfolio Management and Concentration Risk

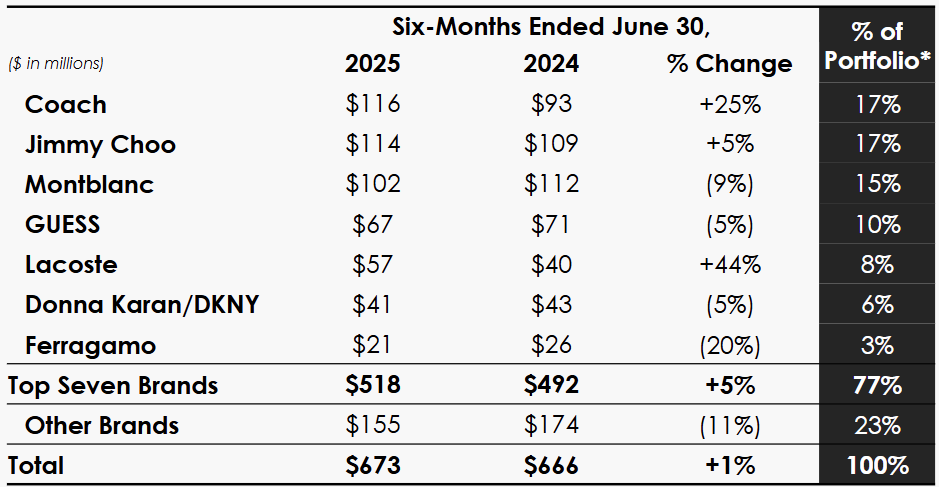

A significant feature of the IPAR model is the high dependence on a select group of leading licenses. Approximately 73% of the company’s total sales revenue is generated by six major brands: Coach, Jimmy Choo, Montblanc, GUESS, Lacoste, and Donna Karan/DKNY. This high revenue concentration makes the renewal of these core licenses the single most critical long-term business risk.

The management strategy focuses on maximizing the value delivered to the licensors throughout the contract term, thereby guaranteeing the highest probability of renewal. This strategy requires constant brand lifecycle optimization, particularly through the disciplined launch of flankers and pillar expansions. For example, in H1 2025, Coach fragrances delivered exceptional growth of 24%, driven by new pillars (Coach For Men Eau de Parfum and Coach Women Gold). Similarly, Lacoste fragrances confirmed a successful acquisition trend with sales surging 42% over the same period. However, the fragility of relying on constant refreshment was highlighted by the 10% decline in Montblanc sales in H1 2025, caused by softening performance in recent flanker lines (Montblanc Legend Red and Legend Blue). This demonstrates that continuous, successful product innovation is essential to justify high-value license renewal terms.

3.2 Strategic Expansion

To mitigate license expiration risk and diversify its IP portfolio, Interparfums is actively pursuing two key strategies: securing ultra-long-term licensing agreements and developing proprietary brands.

In 2025, the company reinforced its portfolio with the acquisition of a long-term license agreement with Maison Longchamp, running until December 31, 2036, with the first product launch scheduled for 2027. This move aligns with the strategy of partnering with emblematic, heritage French fashion brands to secure durable IP.

A more transformative shift is the investment in proprietary IP ownership. IPAR already owns the Rochas brand (acquired in 2015), which is managed through its Spanish distribution subsidiary, Parfums Rochas Spain, SL. Expanding on this, IPAR announced the development of its first new proprietary brand, Solférino, which debuted at the end of 2024 with a collection of ten fragrances. This move signals a partial transition from being purely an “IP renter” to an “IP owner.” By developing and owning the Solférino brand, IPAR bypasses perpetual royalty payments, enabling the company to capture 100% of the gross profit margin. This strategic transition is crucial for increasing the long-term quality of earnings and reinforcing the economic sustainability of the business beyond the reliance on temporary licensing cycles.

IV. Financial Performance

4.1 H1 2025 Sales

Interparfums reported a complex financial picture for the first half of 2025, balancing operational strengths against macroeconomic headwinds. Consolidated net sales for the first six months of 2025 increased year-to-date by 1% (in USD terms). However, Q2 2025 net sales were $333.9 million, representing a 2% decline compared to Q2 2024 ($342.2 million) and falling short of analyst expectations. In euro terms, European-based sales exhibited stronger performance, growing 5.8% in H1 2025 (€446.9 million).

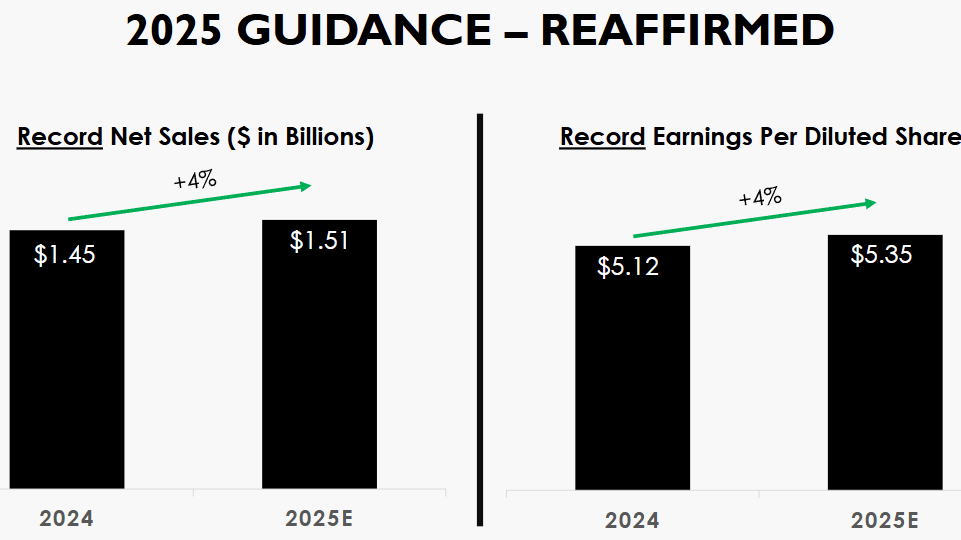

Despite the quarterly miss, management reaffirmed its full-year 2025 guidance, projecting net sales of $1.51 billion and diluted EPS of $5.35. The company relies heavily on a strong performance during the historically crucial holiday season to achieve these annual objectives. This reaffirmation, combined with strong license performance (Coach +24%, Lacoste +42%), indicates that management believes general catalog sales slowdowns experienced in the first half—attributed to consumer hesitation caused by geopolitical turmoil —will be temporary or fully offset by product launches in the second half.

4.2 Margin Expansion and Cost Discipline

A key measure of operational excellence is the consistent Gross Margin expansion. The Gross Margin grew by 170 basis points in Q2 2025, reaching 66.2%, and expanded by 150 basis points year-to-date, reaching 65.0%. This level of margin capture is higher than the company’s historical average of approximately 60.16% (TTM) and demonstrates strong discipline in managing production costs and optimizing the product mix.

However, Q2 Operating Margin declined slightly to 17.7%, a decrease of 1.2% year-over-year. This margin compression, where gross margin improved but operating margin lagged, signals that the company is absorbing higher Selling, General, and Administrative (SG&A) expenses. These increased costs are likely driven by higher marketing investments to support major product launches, costs associated with logistics transitions, and ongoing investment in the business to gain market share in a fragile consumer environment. This strategy prioritizes long-term growth and brand visibility, using the efficiencies gained at the COGS level to fund aggressive investment at the SG&A level.

4.3 Geographic Financial Divergence and FX Impact

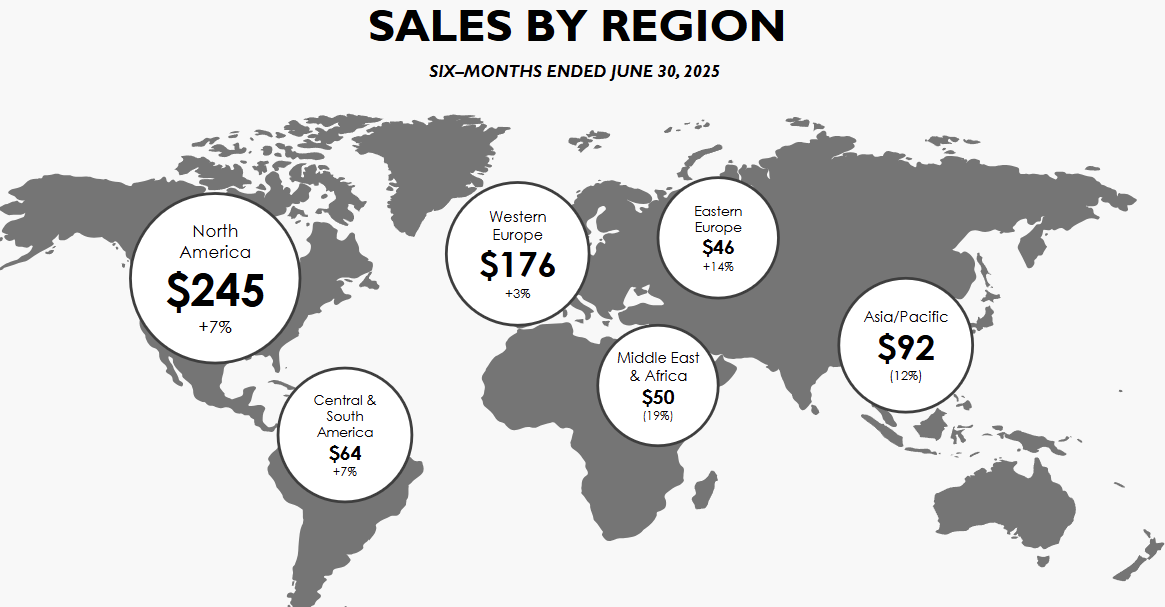

The geographic sales performance in H1 2025 showed significant divergence: Eastern Europe led with 7% growth, followed by the Americas with 7% growth, and Western Europe with 3% growth, while Asia-Pacific sales contracted sharply by 12%.

The robust performance in the Americas and Europe provides stability and confirms the efficacy of premiumization strategies in mature markets. Conversely, the sharp contraction in Asia-Pacific signals significant operational or economic headwinds, likely stemming from reduced luxury consumption or continued adverse impacts on the crucial travel retail sector globally. Stabilizing and reigniting growth in Asia-Pacific remains a necessary long-term objective to access the high-growth affluent middle-class demographic identified in the region.

Foreign currency translation provided a positive influence on reported sales figures. The average dollar/euro exchange rate difference contributed a positive impact of 2.0% on Q2 2025 net sales and 0.4% on H1 2025 net sales, primarily due to the euro’s strengthening relative to the USD year-over-year.

V. Global Distribution Network

5.1 Multi-Channel Wholesale Focus

Interparfums maintains a massive distribution footprint, ensuring global reach by distributing products in over 120 countries. The channel strategy is strictly wholesale-focused, targeting high-end department stores, MCM brand stores, and prestige beauty retailers. Key relationships with major wholesale partners facilitate broad market penetration, notably including Sephora, where the company maintains approximately 65% distribution coverage, and Ulta Beauty, with approximately 55% coverage.

The wholesale model also incorporates reliance on travel retail locations, a segment that was significantly impaired by the curtailment of international air travel post-2020. The recovery and stabilization of global travel retail remain essential for the resumption of high-volume, global growth.

5.2 Digital Integration and E-commerce Strategy

Digital growth is substantially supported by strong performance on major external platforms. Management specifically highlights success in expanding IPAR’s presence on Amazon, alongside traction gained by social commerce platforms like Divabox and TikTok Shop. These channels are viewed as crucial hubs, powered by the reach and engagement capabilities of content creators and influencers across social media.

This reliance on external digital ecosystems is supported by a robust Advertising & Promotion (A&P) investment strategy. IPAR actively commits to continuing to increase A&P spend ahead of top-line growth. This capital is used to finance sell-through at major retailers and simultaneously drive traffic across all distribution channels, integrating both in-store and online engagement. IPAR strategically prioritizes measurable performance marketing over merely maintaining cost ratios, confirming the allocation of capital efficiency derived from higher gross margins directly into consumer engagement. This deliberate strategy emphasizes leveraging platform traffic rather than owning the traffic source, maximizing scale while maintaining capital flexibility.

This approach allows the company to capture the rewards of the e-commerce boom and the consumer shift to digital purchasing, but without incurring the heavy, fixed CapEx burden required for establishing a proprietary global D2C logistics infrastructure. The focus remains on core competencies: IP management and brand marketing.

VI. Conclusions and Long-Term Outlook

6.1 Competitive Moats

Interparfums has established a durable, defensible position in the global luxury fragrance market through several structural advantages. Its operational agility allows for the rapid scaling of successful product launches (e.g., Coach and Lacoste) without being constrained by heavy fixed manufacturing assets. Furthermore, the company possesses deep industry expertise cultivated over 30 years, giving it unparalleled knowledge in balancing the four critical elements of a successful fragrance product: scent, bottle, packaging, and buyer appeal. Finally, IPAR’s longevity and complex network of relationships create significant barriers to entry in the prestige fragrance sector, requiring high capital investment, technical expertise in formulation, and strong, trust-based relationships with licensors—assets few newcomers can replicate.

6.2 Key Risk Factors

The principal risk remains the dependency on a few key licensing contracts, meaning sales are highly concentrated. This vulnerability is being addressed through a dual mitigation strategy: securing licenses with ultra-long terms (like Longchamp extending to 2036) and investing in developing proprietary IP (Solférino).

Financial visibility is affected by Foreign Exchange fluctuation, given that European operations drive 65% of net sales. Currency volatility, particularly the USD/EUR rate, impacts reported earnings. Management mitigates this through portfolio diversification and internal hedging mechanisms.

Lastly, the significant H1 2025 sales contraction in Asia-Pacific (-12%) highlights the sensitivity of the model to geopolitical uncertainty and regional economic slowdowns. The counter-strategy relies on the continued strength and reliability of core licenses in stable markets, such as North America, which delivered 7% growth in H1 2025, while continuing to invest aggressively in product launches to capture market share.

6.3 Long-Term Growth Catalysts

Interparfums’ long-term growth trajectory is supported by a robust pipeline of product innovation focused on expanding core franchises (Montblanc, Jimmy Choo, Coach) and leveraging recent acquisitions (Lacoste, Ferragamo, Abercrombie & Fitch) throughout 2026. The aggressive acquisition of new long-term licenses, exemplified by the Longchamp deal, secures revenue visibility for over a decade. The development of proprietary brands like Solférino represents a structural shift designed to capture 100% of the brand value creation, thereby insulating the business from the inherent risks of licensing cycles.

In summation, Interparfums maintains a specialized, highly durable, and strategically efficient business model. The company’s unique licensing arbitrage, combined with its strong balance sheet, positions it to sustain superior gross margins and continue its path toward generating profitable growth through the strategic deployment of intellectual property and operational agility.

Thanks for reading!

Stiliyan Loukanov, Feather Fund

Open an account with Interactive Brokers:

https://ibkr.com/referral/stiliyan756

Sign up to Revolut with the link below to support the blog:

ttps://revolut.com/referral/?referral-code=stiliyujwu!MAY1-24-AR

Open an account with eToro to support the blog:

Disclaimer: The information presented here, including ideas, opinions, views, predictions, forecasts, commentaries, or suggestions, whether explicitly stated or implied, is intended purely for informational, entertainment, or educational purposes. None of the content should be interpreted as personalized investment or financial advice. Although every effort has been made to ensure the accuracy of the information provided, errors or inaccuracies may be present. Always exercise caution and seek professional financial advice before making any investment decisions.