International Container Terminal Services, Inc. (ICT)

An In-Depth Analysis of the Business Model

Executive Summary

International Container Terminal Services, Inc. (ICT) operates as a high-margin, mission-critical infrastructure provider specializing in the acquisition, development, and management of container terminals globally. The company earns revenue primarily through transactional fees for stevedoring, berthing, and storage services provided to international shipping lines and cargo owners. The economics of ICT are defined by exceptionally high barriers to entry, long-term regulatory protection through 25-to-50-year concession agreements, and a focused “Origin and Destination” (O&D) cargo strategy that reduces exposure to the volatility of transshipment hubs.

The core competitive advantage is ICT’s status as the world’s largest independent terminal operator, ensuring operational neutrality that attracts a diverse customer base across all major shipping alliances. This independence is coupled with a disciplined capital allocation model that generates a return on invested capital (ROIC) significantly exceeding its weighted average cost of capital (WACC). The primary risk remains macroeconomic sensitivity, particularly currency volatility in emerging markets and geopolitical disruptions to trade routes like the Red Sea. ICT is a strategically diversified infrastructure platform that captures a recurring “toll” on global trade through a monopolistic portfolio of gateway assets.

1. What They Sell and Who Buys

ICT provides the physical and digital infrastructure necessary for the seamless transfer of containerized cargo between sea-bound vessels and land-based logistics networks. The company’s output is measured primarily in Twenty-Foot Equivalent Units (TEUs), the standard industry metric for container volume.

Core Services and Operational Mechanics

The company’s service portfolio is highly specialized, requiring massive capital investment in ship-to-shore gantry cranes, rubber-tired gantry cranes, and sophisticated terminal operating systems. The primary service, stevedoring, involves the loading and unloading of containers. This process is highly time-sensitive; shipping lines prioritize terminals that offer superior gross crane productivity to minimize vessel turnaround time, as idle time for a modern Ultra-Large Container Vessel can cost carriers tens of thousands of dollars per day.

Beyond basic handling, ICT provides berthing services, which include the provision of wharfage and mooring infrastructure. A critical high-margin component of the service mix is ancillary services, notably container storage. Terminals charge demurrage fees when containers exceed their “free time” in the yard. During periods of supply chain inefficiency or congestion, these storage revenues often increase, providing a counter-cyclical hedge to volume volatility.

Customer Profile and Market Dynamics

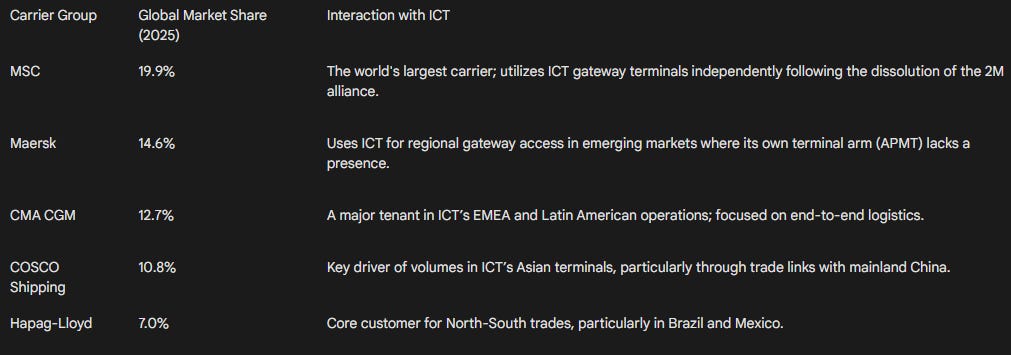

ICT’s customer base consists of the global container shipping elite, organized into massive vessel-sharing alliances. The customer profile is heavily concentrated among the top ten global carriers, who control roughly 85% of global capacity.

The primary buying motivation for these carriers is geographic necessity and operational efficiency. Gateway ports like the Manila International Container Terminal (MICT) or Contecon Guayaquil serve as the sole efficient entry points for their respective hinterlands. Once a carrier includes a port in its weekly "loop", switching costs are prohibitive because of the integrated nature of inland trucking and rail connections.

2. Revenue Model

ICT operates a transactional, usage-based revenue model that essentially functions as a private tax on the movement of goods. The company does not take ownership of cargo; instead, it monetizes its status as a “toll-gate” for international trade.

Pricing Power and Value Capture

Value capture is achieved through a combination of regulated tariffs and commercial negotiations. In many of ICT’s key markets, such as the Philippines, tariffs for domestic and international cargo are set or approved by the government. These tariffs are often inflation-linked, allowing the company to maintain margins even in inflationary environments. In more competitive transshipment markets, pricing is negotiated based on volume commitments, but ICT’s focus on gateway cargo (O&D) provides superior pricing power compared to pure transshipment hubs.

The revenue model is strictly transactional. Every time a crane moves a container, a fee is generated. This ensures that ICT scales directly with the growth of global trade and regional GDP. The high-margin nature of storage fees, which require minimal incremental operating expense once the land is developed, allows for significant “margin accrual” during periods of high terminal utilization.

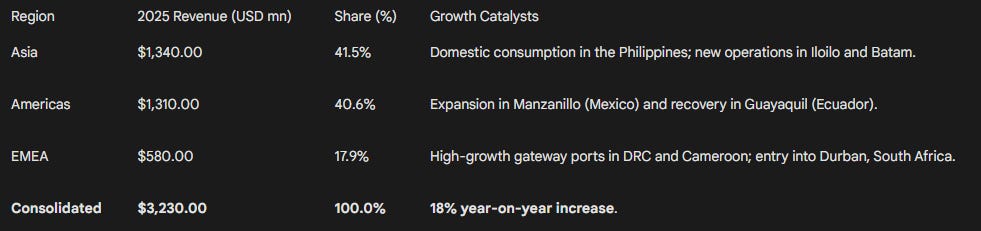

Revenue Segmentation and Regional Contribution

ICT has successfully diversified its revenue stream across three main geographical pillars, reducing dependence on any single economy.

The nearly equal split between Asia and the Americas provides a unique balance; when trade between Asia and the US slows, intra-Asian trade or South American agricultural exports often compensate.

3. Revenue Quality

The quality of ICT’s revenue is defined by its long-term predictability and the “captive” nature of its cargo base. Unlike typical service businesses, ICT’s revenue is protected by legal frameworks that span decades.

Predictability and Stability

The primary engine of stability is the concession agreement. These contracts, typically granted by port authorities or national governments, provide ICT with exclusive operating rights for 25 to 50 years. For example, the MICT contract in Manila extends to 2038, and the VICT contract in Melbourne was recently extended to 2066. This creates a high-visibility revenue “tail” that is essentially guaranteed as long as the terminal remains operational and compliant with regulatory standards.

The focus on O&D cargo further enhances revenue quality. O&D cargo is destined for the local hinterland and must pass through the gateway port. This is structurally different from “transshipment” cargo, which can be easily moved to a competing hub. By dominating gateway ports, ICT ensures that its volumes are driven by the local economy’s health rather than the whims of a shipping line’s network planner.

Concentration and Macro-Sensitivity

While specific customer concentration (percentage of revenue from the top 5 carriers) is not explicitly disclosed in the 2025 audited reports, the nature of the industry suggests that the top alliances account for a significant share of volume. However, ICT mitigates this by serving all alliances simultaneously. If one alliance loses market share to another, the volume typically stays at the ICT terminal, merely changing the “label” on the ship.

The primary threat to revenue quality is currency translation. In 2025, the company reported “unfavorable foreign exchange translation impact” due to the depreciation of the Mexican Peso, Brazilian Real, and Australian Dollar. While the underlying business is often USD-denominated or USD-linked, the translation of local currency results into USD for reporting purposes can create non-operational volatility in the top line.

4. Cost Structure

The terminal operations business is characterized by high operating leverage, where a high proportion of fixed costs means that incremental revenue flows heavily to the bottom line.

Key Cost Drivers

ICT’s cost base is primarily composed of labor, concession fees, and power.

Fixed vs. Variable Split: Approximately 70-80% of costs are fixed or “step-variable”, including depreciation, core administrative staff, and minimum guaranteed concession fees. Variable costs (20-30%) include vessel-linked labor, fuel for yard equipment, and power for reefer containers.

Concession Fees: A significant portion of ICT’s “cost of sales” is the share of gross revenue paid to port authorities. In the Philippines, this is a direct 20% “tax” on revenue, which effectively turns a fixed asset into a variable cost, providing some margin protection during volume downturns.

Manpower Costs: Labor accounted for a substantial portion of the 11% increase in cash operating expenses in 2025. This was driven by higher volumes and “government-mandated and contracted salary rate adjustments” in markets like the Philippines and Mexico.

Margin Progression and Efficiency

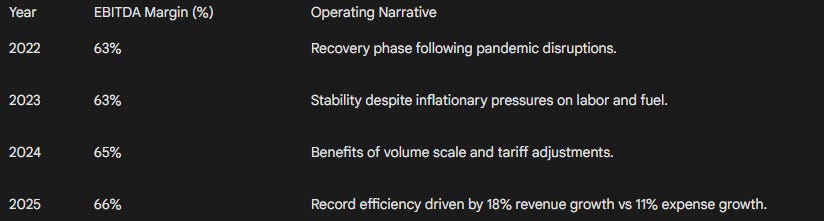

ICT maintains industry-leading operational efficiency, as evidenced by its EBITDA margin expansion.

The mechanism behind this margin expansion is the “digestion” of fixed costs. As TEU throughput increased by 11% in 2025, the fixed costs of gantry cranes and terminal infrastructure were spread over a larger volume base, reducing the “cost per move” and driving the 21% increase in consolidated EBITDA.

5. Capital Intensity

ICT’s business model requires significant, ongoing capital investment to maintain its competitive position and capture market growth.

Asset Requirements and Balance Sheet Structure

The company’s balance sheet is dominated by long-lived, illiquid assets. As of 2025, Noncurrent Assets exceeded $6.0 billion, primarily split between Intangibles (concession rights) and Property and Equipment (cranes and civil works). The high “Intangible” balance reflects the upfront fees paid to governments to secure multi-decade operating rights, which are then amortized over the life of the contract.

CapEx Dynamics

CapEx is categorized into maintenance (sustaining existing capacity) and expansion (growing the footprint).

While a 20%+ CapEx-to-revenue ratio is high, it is largely discretionary. In periods of economic stress, ICT has demonstrated the ability to "slash capital expenditure to the bare bone", as it did in early 2020, to preserve liquidity.

Cash Conversion and Working Capital

ICT operates with a highly efficient cash cycle, often achieving a negative Cash Conversion Cycle (CCC). Shipping lines are generally billed in USD and required to pay within 20-30 days to avoid service disruptions. Conversely, ICT’s payables to port authorities and equipment suppliers are often on longer terms. This creates a “float” that funds operational requirements.

FCF Generation

Despite the high CapEx, the company generates substantial FCF. In the first half of 2024, ICT reported FCF of $602 million, representing a 24% year-on-year increase. This cash engine allows the company to fund most of its expansion projects through internal cash flow, keeping its net gearing and debt-to-EBITDA ratios well within conservative limits.

6. Growth Drivers

ICT’s growth trajectory is powered by a combination of organic volume recovery, disciplined pricing power, and an aggressive M&A pipeline.

Primary Levers of Growth

Structural Volume Growth: Consolidated throughput hit 14.5 million TEUs in 2025, an 11% increase. This is driven by the durable trend of containerization in emerging markets. As economies in Africa, Southeast Asia, and Latin America mature, goods that were previously shipped as “bulk” are increasingly being containerized.

Pricing Power and Mix Shift: The company achieved 18% revenue growth on 11% volume growth. The 7-percentage-point delta is explained by “tariff adjustments, a more favorable container mix, and higher ancillary service revenues”. ICT has a proven ability to push through price increases that at least match local inflation.

New Concessions (Inorganic): The entry into the Port of Durban (South Africa) in 2025 is a transformative growth catalyst. As the largest container terminal in Africa, the 25-year joint venture provides a massive new volume base starting in 2026. Similarly, the Batam (Indonesia) acquisition adds 900,000 TEUs of handling capacity.

Growth Constraints and Execution Risk

The single biggest constraint is the regulatory bottleneck. Winning a port concession is a multi-year, highly political process. Any delay in government approvals or changes in local maritime policy can stall the expansion pipeline. Execution risk is also elevated in new markets like South Africa, where ICT must navigate complex labor dynamics and integration with state-owned enterprises.

7. Competitive Moat

ICT possesses a “Wide Moat” characterized by localized monopolies and structural independence in an industry plagued by vertical integration conflicts.

Sources of Economic Protection

Regulatory/Legal Monopoly: Port concessions are “finite licenses for essential land”. Once ICT secures the exclusive right to operate a city’s primary gateway, it is virtually impossible for a competitor to enter the market. The high capital cost and geographic scarcity of deep-water berths act as a natural “fortress”.

Independence (The Neutrality Moat): Major shipping lines (Maersk, MSC, CMA CGM) have their own terminal subsidiaries. However, a carrier is often reluctant to use a terminal owned by its direct competitor to avoid giving them data or priority access. ICT, as an independent operator, is the “Switzerland” of ports. It can serve all carriers equally, allowing it to achieve higher utilization rates than carrier-owned terminals.

Switching Costs: Once a port is integrated into a global trade “string”, the logistics of moving to another port, including renegotiating thousands of trucking contracts and rail schedules, are so complex that carriers only switch in extreme circumstances.

Evidence of Durability and Capital Efficiency

The durability of the moat is best expressed through the company’s Return on Invested Capital (ROIC) relative to its cost of capital.

The data for 2025 reflects a highly value-accretive business model:

ROIC (TTM): 18.6% to 21.3%.

WACC: Estimated at 6.84%.

Economic Spread: ~12-14%.

A company that consistently earns double its cost of capital over five years, as ICT has done, is by definition protected by a significant moat.

Moat Assessment: Widening

The moat is currently widening. ICT is leveraging its strong balance sheet to secure new, longer-term concessions (like the Durban and Batam projects) and extending existing ones (like Melbourne and Subic Bay). Furthermore, the company’s “Green Port” initiatives and investment in digitalization (e.g., AI-driven terminal optimization) are creating a technological barrier that smaller, less-capitalized regional operators cannot match. ICT is not just buying ports; it is institutionalizing the “toll-road” model on a global scale.

Thanks for reading!

Stiliyan Loukanov, Feather Fund

Open an account with Interactive Brokers:

https://ibkr.com/referral/stiliyan756

Sign up to Revolut with the link below to support the blog:

ttps://revolut.com/referral/?referral-code=stiliyujwu!MAY1-24-AR

Open an account with eToro to support the blog:

Disclaimer: The information presented here, including ideas, opinions, views, predictions, forecasts, commentaries, or suggestions, whether explicitly stated or implied, is intended purely for informational, entertainment, or educational purposes. None of the content should be interpreted as personalized investment or financial advice. Although every effort has been made to ensure the accuracy of the information provided, errors or inaccuracies may be present. Always exercise caution and seek professional financial advice before making any investment decisions.