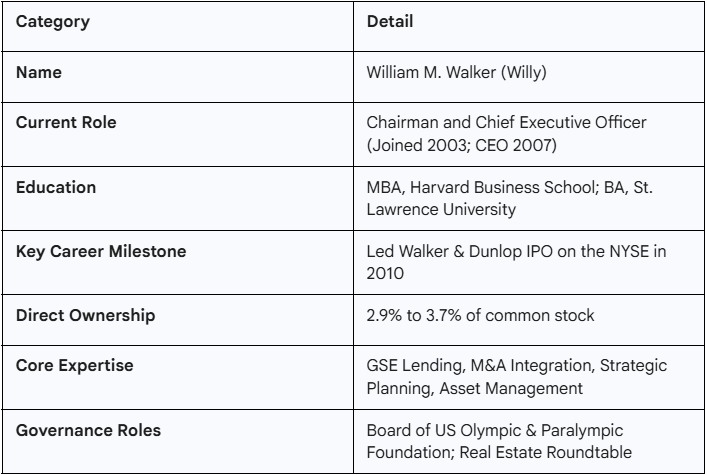

CEO Profile: William M. Walker, Walker & Dunlop

An Evaluation of Willy Walker’s tenure as CEO of W&D

Executive Summary

The transition of Walker & Dunlop (W&D) from a regional, family-owned mortgage banking firm founded during the Great Depression into a premier national commercial real estate (CRE) finance and advisory powerhouse is inextricably linked to the eighteen-year tenure of William M. Walker as CEO. Since assuming the leadership role in 2007, he has steered the organization through a strategic evolution focused on scaling the mortgage servicing and asset management segments to create a durable, recurring revenue base that buffers the cyclicality of the brokerage business. Here, we provide a detailed examination of management’s career trajectory, decision-making record, and alignment with the shareholders.

The analysis identifies a leadership profile characterized by aggressive yet disciplined capital allocation, particularly in the realm of M&A. Significant milestones include the 2009 acquisition of Column Guaranteed, which provided the scale necessary for the firm’s 2010 IPO, and the 2012 acquisition of CWCapital, which doubled the size of the servicing portfolio. More recently, the acquisitions of Alliant Capital in 2021 and GeoPhy in 2022 represent a strategic pivot toward affordable housing tax credit syndication and technology-driven valuation services, respectively.

While management has a proven record of meeting scale-oriented targets, such as achieving top-tier rankings as a Fannie Mae, Freddie Mac, and HUD lender, the current macroeconomic environment, termed “The Great Tightening” by management, has presented substantial headwinds to profitability targets. The 2024 diluted EPS of $3.19 and transaction volumes of $40 billion remain well below the peak levels required to meet the original 2025 objectives. Despite these challenges, shareholder alignment remains high, underpinned by the CEO’s equity stake of 2.9% to 3.7% and a compensation structure that is over 85% variable and performance-based.

The following dossier concludes that the CEO represents a long-term steward who has successfully institutionalized a once-private family firm. While the delay in achieving the “Drive to ‘25” financial targets poses a short-term risk to sentiment, the underlying growth in assets under management (AUM) and the resilience of the servicing portfolio suggest a management team focused on sustainable value creation.

CEO Profile at a Glance

Synthesized Assessment

The CEO’s primary strengths lie in institutionalizing corporate strategy through high-accountability “Drive” plans and executing transformative M&A that provides non-linear growth. By prioritizing the lending and servicing side of the business over pure brokerage, management has captured the higher margins and recurring revenue associated with Mortgage Servicing Rights (MSRs). Furthermore, the CEO’s high transparency and extensive media presence have built a strong corporate brand that facilitates talent recruitment from much larger competitors like JLL and CBRE.

Material risks are predominantly concentrated in the firm’s reliance on Government-Sponsored Enterprises (GSEs) and the sensitivity of transaction volumes to the interest rate environment. The firm’s credit risk is largely isolated to its “at-risk” multifamily servicing portfolio, where defaults have trended upward as of late 2025. Additionally, the aggressive nature of recent technology acquisitions like GeoPhy carries integration and earn-out risks if the tech-enabled businesses do not scale as projected.

One-line Verdict

Long-term steward with a demonstrated record of scaling operations and high alignment with shareholder value.

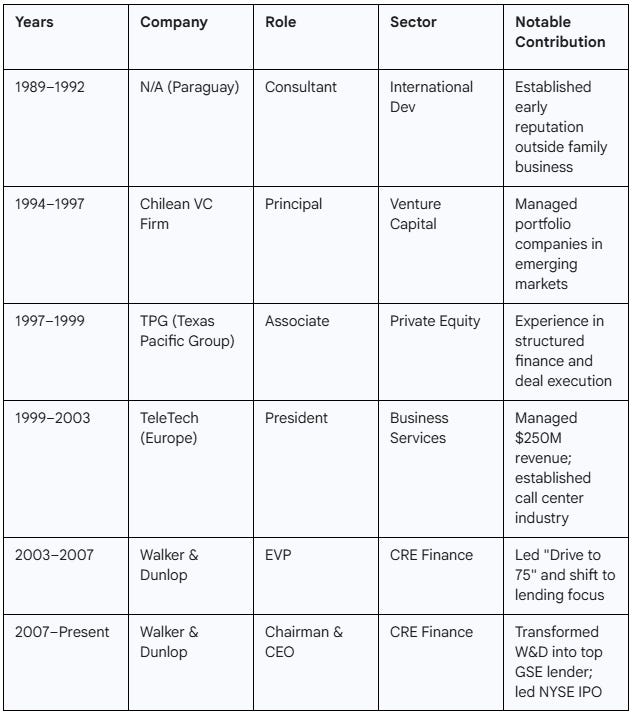

Career Map & Expertise

The professional evolution of William M. Walker is marked by a deliberate period of “external validation” before entering the family business. This background provided him with a management toolkit rooted in international business services and venture capital rather than traditional mortgage banking, which appears to have influenced his focus on operational scale and data-driven decision-making.

Timeline of Roles

Leadership Classification

William is classified primarily as an Operator-Allocator. While his early career at TeleTech demonstrated high-level operational capabilities in managing a $250 million revenue division, his tenure as CEO has been defined by the disciplined allocation of capital toward strategic M&A and the recruitment of brokerage teams. He has effectively moved the firm from a 45th place ranking among CRE lenders in 2007 to 9th by 2009, and eventually to a top-3 ranking in the multifamily space, demonstrating a mastery of scaling professional service organizations.

Core Expertise & Skills

A critical skill identified in William’s track record is the ability to leverage government-sponsored programs (Fannie Mae DUS, Freddie Mac Optigo, HUD) to create a moat. Under his leadership, W&D has consistently maintained its status as a top-tier DUS lender, which allows the firm to underwrite and fund loans without prior approval from Fannie Mae, provided they share in the credit risk. This expertise extends to federal housing policy advocacy, as evidenced by his testimony and media engagement regarding GSE reform and the validation of multifamily lending during market stress.

Additionally, William has spearheaded a technological transformation, moving W&D beyond traditional brokerage. The acquisition of GeoPhy and the development of the “Apprise” tech-enabled appraisal business reflect an expertise in identifying technological disruptors that can improve broker productivity.

Track Record of Decisions

Management’s decision-making history shows a consistent pattern of counter-cyclical aggression. By acquiring competitors or new capabilities during market downturns, the firm has emerged from crises with significantly expanded market share.

Major Decision Table

Decision Patterns

William demonstrates a clear pattern as a Disciplined Allocator focused on high-margin, recurring revenue. Every major acquisition has served to either double the servicing portfolio or add a new, fee-based business line (e.g., affordable housing syndication with Alliant). This strategy has effectively transformed W&D from a “transaction-dependent” firm into one where consistent revenues from Servicing and Asset Management (SAM) segments contribute over half of the total revenue during market slowdowns. The use of structured earn-outs, as seen in the GeoPhy and Alliant deals, further indicates a risk-mitigation strategy where payment is contingent on the achievement of long-term goals.

Ownership & Alignment

Alignment between the CEO and long-term shareholders is robust, characterized by significant direct equity ownership and a compensation program that penalizes underperformance in core financial metrics.

Ownership and Insider Activity

Management’s direct ownership of approximately 2.9% to 3.7% of the company’s outstanding common stock—valued between $59 million and $77 million—is a primary alignment factor. Internal guidelines require the CEO to maintain stock ownership equal to at least five times his base salary, a threshold William significantly exceeds.

Insider trading history shows a narrative of long-term retention. While some shares have been sold for tax purposes or diversification, William has also participated in opportunistic open-market buying. Notably, in March 2025, he purchased $1.5 million worth of shares at $86.80, a price above the subsequent market lows, signaling high confidence in the long-term intrinsic value of the firm.

Compensation Impact and Dilution

The compensation structure for the CEO is roughly 86.8% variable, with only 13.2% comprised of base salary. Long-term incentive awards are tied to aggregate total revenues, average diluted EPS, and return on equity (ROE) over three-year performance periods. This structure ensures that management is only compensated at top-tier levels when shareholders also experience growth in book value and earnings.

Dilution management has been balanced. While major acquisitions like CWCapital were financed with significant stock issuance (approx. 34% of the firm at the time), the resulting growth in the servicing portfolio and EPS eventually offset the dilutive impact. More recent acquisitions like Alliant used a mix of cash, stock, and earn-outs to minimize immediate dilution.

Alignment Rating: High

Governance, Candor & Risks

Governance at W&D is marked by a clear commitment to transparency, though the dual role of Chairman and CEO warrants oversight by a strong lead independent director.

Evidence of Candor and Media Reputation

William is regarded in the business press (CNBC, Bloomberg, WSJ) as a serious, data-driven commentator on the CRE industry. His “Walker Webcast” has become a primary channel for communicating market insights and company strategy to both clients and investors. In earnings communications, management has been candid about the challenges of the “Great Tightening”. For example, in the 2024 Annual Report, management explicitly acknowledged that macroeconomic conditions had slowed the rate of growth toward the “Drive to ‘25” targets, rather than attempting to “spin” the results.

Controversies and Lawsuits

The firm has maintained a relatively clean regulatory record. Minor litigation, such as the 2013-2016 CA Funds Group lawsuit involving a breach of contract claim over fund marketing fees, was resolved via summary judgment in favor of the defendants. No evidence of significant regulatory sanctions, NGO warnings, or governance scandals was found in the review of SEC filings and business media.

Promises vs. Results

As an analyst focused on long-term stewardship, evaluating the gap between management’s stated targets and realized outcomes is paramount. William’s tenure is defined by his use of five-year strategic cycles, which provide a quantitative ledger of management’s reliability.

Credibility Assessment

Since 2007, management has launched three major strategic initiatives: the “Drive to 75” (2007–2012), the “Drive to ‘20” (2016–2020), and the “Drive to ‘25” (2021–2025). The first two were largely successful in their scale objectives, transforming W&D into the #1 Fannie Mae lender and expanding revenue five-fold. However, the “Drive to ‘25” has encountered significant friction. While the firm successfully hit its AUM goal ($18.4 billion vs. $10 billion target) and established the affordable housing platform through the Alliant acquisition, the profitability and volume targets are currently behind schedule.

Takeaway: Management has high credibility for scaling market share and integrating M&A but has been over-optimistic regarding the duration of the low-interest-rate environment, leading to a likely miss on original 2025 EPS targets.

Shareholder Alignment Report

Methodology: Alignment Framework

The evaluation of alignment is categorized into seven dimensions that quantify the relationship between the CEO and long-term shareholders.

Economic Ownership: Direct stake size relative to peers and guidelines.

Compensation Alignment: Ratio of fixed vs. variable pay and use of long-term metrics.

Insider Trading Behavior: Pattern of buying/selling relative to market performance.

Dilution & Shareholder Treatment: Discipline in share issuance and commitment to buybacks and dividends.

Capital Allocation Discipline: ROE focus and M&A integration success.

Related-Party Transactions: Transparency regarding family/insider business deals.

Governance & Candor: Clarity of communication and responsiveness to market shifts.

Verdicts are defined as Aligned (interests synchronized), Misaligned (management interests prioritized), or Mixed (significant conflicts or trade-offs present).

Category 1: Economic Ownership

Economic ownership is the most significant indicator of alignment at W&D. Unlike many “professional” CEOs who view their role as a high-paying job, William acts as a primary stakeholder. With a stake of 2.9% to 3.7%, he is among the largest individual shareholders in the firm.

Verdict: Aligned.

Category 2: Compensation Alignment

The Compensation Committee has structured William’s pay to be heavily weighted toward performance. In 2024, approximately 86.8% of his $7.58 million total compensation was “at risk,” consisting of bonuses and equity awards that only vest based on company earnings performance.

Narrative: The transition from a “Drive to ‘20” plan to the “Drive to ‘25” plan involved the creation of new equity incentive plans (2020 and 2024 Equity Incentive Plans) that set challenging hurdles for EPS and ROE. Because a significant portion of the CEO’s compensation is based on adjusted core EPS, which removes non-cash revenues, he is incentivized to focus on cash-flow generation.

Verdict: Aligned.

Category 3: Insider Trading Behavior

Management’s insider trading behavior is marked by a “net accumulation” trend. There are no patterns of frequent, automated sells that often suggest a lack of confidence in the stock’s appreciation potential.

Verdict: Aligned.

Category 4: Dilution & Shareholder Treatment

W&D has utilized its stock as a “currency” for growth, particularly in the 2012 CWCapital acquisition and the 2021 Alliant acquisition. While this causes short-term dilution, the long-term result has been a massive expansion in the servicing portfolio, the “crown jewel” of the business that provides stable cash flows.

Analysis: Management has offset the impact of dilution by maintaining a consistent dividend policy. The board raised the dividend by 3% in early 2025, even while EPS was under pressure, reflecting a commitment to returning capital to those who hold through cycles.

Verdict: Mixed.

Category 5: Capital Allocation Discipline

The CEO’s capital allocation has been surgical. He has prioritized acquisitions that add MSRs, which act as a hedge during high-rate environments because the loans are high-quality, government-backed multifamily mortgages that are unlikely to prepay rapidly when rates are high.

Verdict: Aligned.

Category 6: Related-Party Transactions

As the grandson of the founder, the CEO is part of the “Walker” legacy. However, the firm has successfully transitioned to an institutional governance model. Related-party disclosures in the proxy statements are standard for a firm of its size, typically involving registration rights agreements and investments in the firm’s own investment funds. No evidence exists of the CEO utilizing company funds for personal benefit or excessive family perks.

Verdict: Aligned.

Category 7: Governance & Candor

William maintains high visibility and candor, which is reflected in his market commentary. He has been clear about the firm’s credit quality, stating that 91% of multifamily loans are fixed-rate, which limits the credit risk during rate hikes.

When the “Drive to ‘25” targets became clearly unattainable in their original timeframe due to the Federal Reserve’s rate hikes, management did not hide behind accounting changes. They acknowledged being “off course” and shifted focus to scaling AUM and technology, which are less rate-sensitive in the long term.

Verdict: Aligned.

Cross-Sectional Patterns & Benchmarking

Synthesized Alignment Theme

The overarching theme of the current leadership is “The Institutionalized Owner.” The CEO has successfully merged the long-term horizon of a family business with the accountability and transparency required of a public NYSE firm.

One identified contradiction is the tension between the firm’s aggressive “Drive to ‘25” growth targets and its reputation for disciplined, low-risk underwriting. Achieving $13 EPS in a high-interest environment proved an unachievable target. The decision to prioritize credit safety over hitting the EPS target is a hallmark of long-term shareholder alignment, even if it results in a short-term “miss” against management’s own guidance.

Final Assessment

The evaluation of William M. Walker’s tenure as CEO of Walker & Dunlop reveals a leader who has demonstrated exceptional discipline in navigating multiple market cycles. His strategy of using five-year “Drive” plans has provided the firm with a clear roadmap for scale, and his ability to execute large-scale, transformative acquisitions has consistently elevated the company’s competitive position within the GSE lending ecosystem.

Conclusion: This CEO is highly aligned with long-term shareholder value and shows evidence of disciplined stewardship.

Thanks for reading!

Stiliyan Loukanov, Feather Fund

Open an account with Interactive Brokers to support the blog:

https://ibkr.com/referral/stiliyan756

Sign up to Revolut with the link below to support the blog:

ttps://revolut.com/referral/?referral-code=stiliyujwu!MAY1-24-AR

Open an account with eToro to support the blog:

Disclaimer: The information presented here, including ideas, opinions, views, predictions, forecasts, commentaries, or suggestions, whether explicitly stated or implied, is intended purely for informational, entertainment, or educational purposes. None of the content should be interpreted as personalized investment or financial advice. Although every effort has been made to ensure the accuracy of the information provided, errors or inaccuracies may be present. Always exercise caution and seek professional financial advice before making any investment decisions.